-

Content

Last Updated on June 3, 2025 by Robert Luong

If you've ever received a direct deposit for your paycheck, or transferred money between bank accounts, chances are you've used ACH online payments. For businesses, ACH transfers provide a secure, cost-effective way to handle transactions without relying on paper checks or expensive wire transfers.

In this guide, we'll cover everything you need to know about ACH transfers, including how they work, processing times, how they compare to wire transfers, and how to set them up for your business.

What is an ACH transfer?

ACH network stands for Automated Clearing House network. It’s used by banks in the U.S. to move money electronically between banks and financial institutions.

For businesses, ACH transfers are a cheap and easy way to get paid without needing a physical card, cash, or checks. It can work in two ways: as an ACH credit (sender pushes money to recipient account) or an ACH debit (recipient pulls money from sender account). Read more about the difference between ACH credit and ACH debit here.

If you're from Canada, you may be thinking, “ACH transfer sounds a lot like an Electronic Funds Transfer (EFT).” You’re not wrong. An EFT is essentially the same thing, just the Canadian version.

What are the differences between Wire, SWIFT, EFT, and ACH transfers?

If you’ve ever tried to send or receive money electronically, you’ve probably come across terms like ACH, Wire, SWIFT, and EFT. They all refer to ways of moving funds between banks, but they’re not the same. Let’s break them down:

- ACH (Automated Clearing House) transfers: ACH uses a centralized U.S. payment network to move money in batches.

- EFT (Electronic Funds Transfer) transfers: EFT works like ACH. It’s used to transfer money between Canadian bank accounts.

- Wire transfers: Wires transfers use the SWIFT payment network (not a transfer method) to send payments between banks across borders. If you send money overseas using a wire transfer, it probably goes through SWIFT.

| Difference | ACH transfers | EFT transfers | Wire transfers |

|---|---|---|---|

| Region | United States | Canada | Global (domestic and international) |

| Speed | 2–5 business days | 2–5 business days | Same day (domestic) or 1–2 days (international) |

| Cost | 0.5%–1% per transaction (often capped at $3–$6) | 0.5%–1% per transaction (often capped at $3–$6) | $10–$50 or more per transfer |

| Reversibility | Yes (under certain conditions) | Yes (under certain conditions) | No (once sent, cannot be reversed) |

| Used for | Payroll, recurring billing, invoice payments, etc. | Payroll, recurring billing, invoice payments, etc. | Large and cross-border transactions |

If you need a cost-effective way to process recurring payments or payroll, ACH is the way to go. If you need to transfer large sums quickly, wire transfers might be your better choice.

What are examples of ACH transfers?

You might not know the term “ACH transfer,” but you’ve almost certainly used one. Here are some everyday examples:

- ACH direct deposit: Most employers use ACH to deposit paychecks straight into employee banks or credit unions.

- Bill payments: The customers might use ACH to pay bills automatically each month, such as utilities, insurance, and subscription services.

- Government payments: Tax refunds, social security, and other government benefits are usually sent by ACH transfers.

- Bank-to-bank transfers: Moving money between your checking and savings accounts at different banks also uses the ACH network.

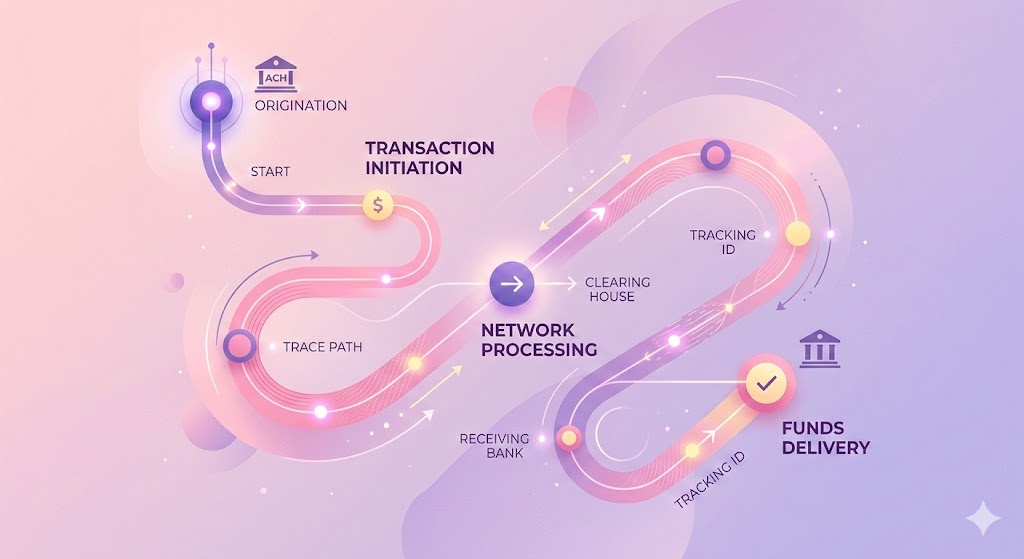

How do ACH transfers work?

ACH payments work through a multi-step process to ensure a secure and accurate money transfer between accounts.

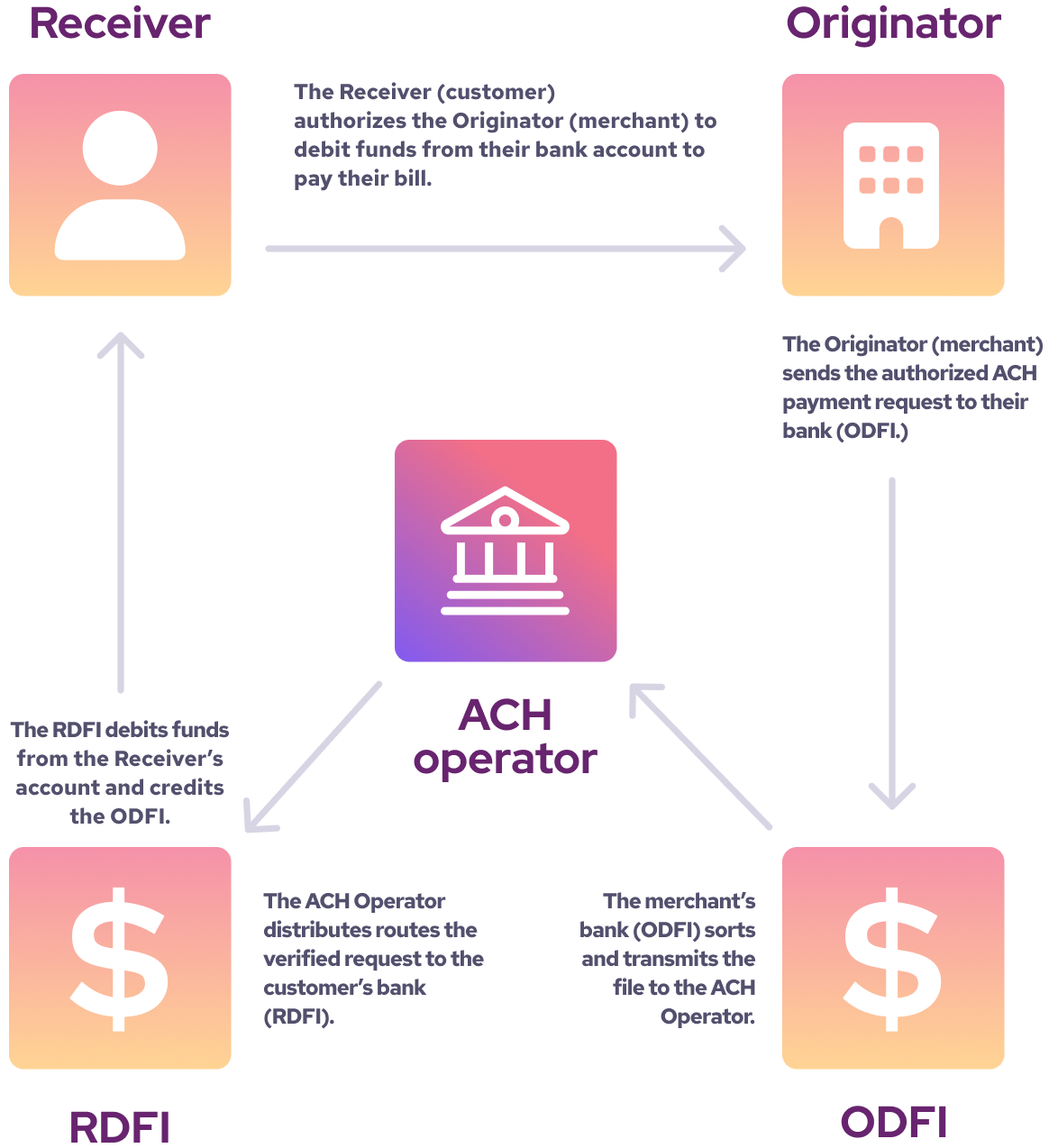

The scope of this section focuses on how a recipient (seller or merchant) collects ACH payments from their customers. Here's how the process unfolds:

1. Initiation

First, you create an ACH authorization form and get your customer's signature. This form includes their account number and routing number. It gives you permission to pull funds (an ACH debit transfer) from their checking account either one-time or ongoing for recurring payments. Learn the difference between ACH debit and ACH credit here.

2. Submission to the ACH network

With this authorization, when the payment is due, you (or your payment processor) send the ACH debit request to the network. This includes the customer’s banking info and the transaction amount. The ACH network will verify the transaction details to ensure they are accurate and properly formatted. The ACH network acts as a middleman who follows the payment instructions and routes the transaction between the payer’s and recipient’s banks.

3. Batch processing

Instead of transferring each transaction to your bank account one by one—which would be costly and time-consuming for the network, your ACH transactions within that business day are grouped and settled in batches at the end of the day.

4. Clearing and settlement

The ACH network checks that the payment details are valid and that the payer has enough funds in their account. If everything checks out, the funds are transferred from the payer’s bank to the recipient’s bank.

However, sometimes an ACH payment doesn’t go through. This is called an ACH return, and it typically happens due to insufficient funds, incorrect account details, or unauthorized transactions.

5. Completion

Your bank receives the funds and deposits them into your business account. This usually takes 2–5 business days, depending on your processor and bank.

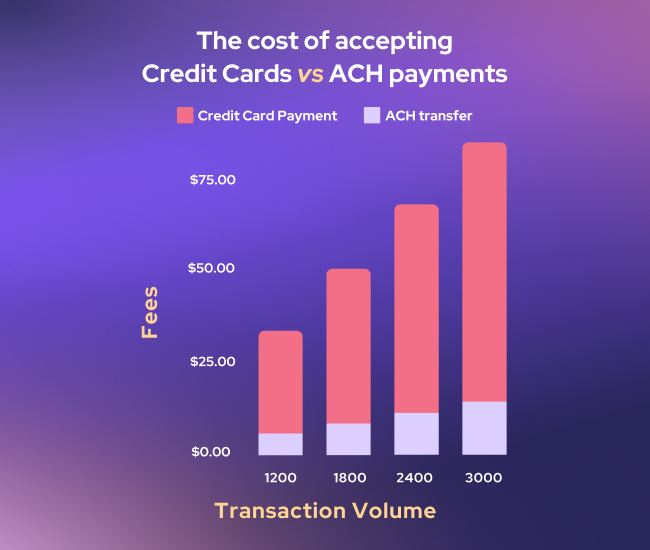

How much do ACH transfers cost?

ACH transfers usually cost between 0.5% and 1% per transaction, which is significantly lower than credit card payments, 1.8% to 3%. Many payment processors also cap the fee, often around $3 to $6 per transaction.

That’s why ACH is a popular choice for businesses collecting large invoices, recurring payments, or B2B payments. Below is a full comparison of ACH transfer fees charged by popular processors.

| ACH processing company | Processing fees |

|---|---|

| Helcim | 0.5% + 25¢ per transaction Fee capped at $6 per transaction |

| Stripe | 0.8% per transaction Fee capped at $5 per transaction |

| Square | 1% per transaction (minimum $1) |

| GoCardless | Domestic: 0.5% + $0.05 (cap $5) to 0.75% + $0.05 (cap $6.25) International: 1.75% + $0.40 to 2% + $0.40 |

| Rotessa | $17/month to $95/month (tiered by volume) 35¢/transaction for 250–1,000 monthly transactions Custom pricing for 1,000+ monthly transactions |

When should you use ACH transfers?

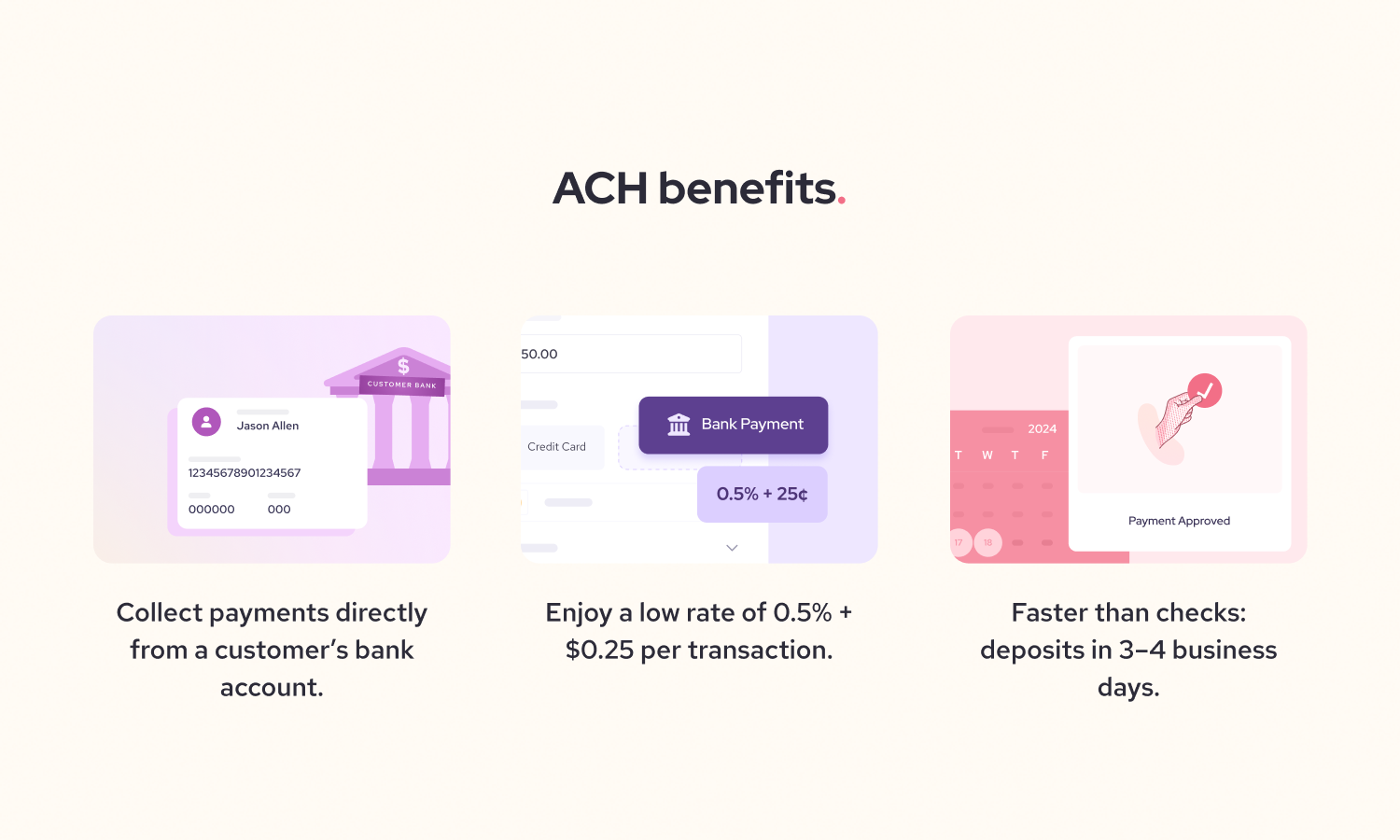

You should use ACH transfers if you’re looking for a cost-effective way to get paid. ACH payments are cheaper than credit card ones. For example, Helcim’s merchants enjoy a low rate of 0.5% + $0.25 per transaction, capped at $6 for transactions under $25,000. If your business offers high-ticket products or services, you can save lots of processing fees with ACH transfers.

If you use recurring billing software with ACH, the payments are collected automatically every billing period. This means, your customers don’t need to manually enter payment details. Besides, ACH transactions are governed by strict rules set by NACHA and financial regulators, so you can avoid ACH fraudulent transactions and ensure the safety of your customers and business.

What types of businesses should use ACH transfer?

ACH transfers are ideal for businesses that process payments regularly in the repeating billing periods. Below are the top 10 industries that adopt ACH transfers the most:

| Industry | Percentage of Transactions Paid with ACH (%) |

|---|---|

| Platforms Apps and SaaS | 8.91% |

| Organizations and Associations | 7.47% |

| Contractors Home Services | 6.14% |

| Professional Services | 4.53% |

| HotelsLodging | 4.49% |

| Financial Institution | 4.07% |

| Education | 3.73% |

| Transportation | 2.65% |

| Government | 1.69% |

| Wholesale | 1.63% |

Businesses that rely on recurring payments like gyms, streaming services, and membership-based businesses can benefit greatly from ACH transfers. Once the customers sign an ACH authorization form, payments are processed automatically. Over time, recurring charges can add up to significant amounts, and the lower fees associated with ACH transfers can save merchants lots of money compared to credit cards.

Businesses that deal with large invoice payments like law firms, real estate businesses, accounting firms, wholesale, or manufacturing can benefit from the affordable rates of ACH payments.

How long do ACH transfers take to process?

ACH transfers typically take 1-5 business days, depending on the type of transfer, the bank, and your payment provider. Here are some common timelines you’ll see promised:

- Standard ACH transfers: These usually take 1-5 business days.

- Next-day ACH transfers: Some banks and payment processors offer expedited ACH transfers, typically processed within 24 hours. These services typically involve additional fees. For example, Square offers next-business-day ACH transfers for a fee of 1.75% per transaction, which is at least three times higher than standard fees.

What banks do ACH transfers?

Most major banks and financial institutions in the United States support ACH transfers, some of the big ones include:

- Chase

- Bank of America

- Wells Fargo

- Citibank

- U.S. Bank

Often banks will charge fees for outgoing ACH transfers, while incoming transfers are free. However, if you’re a business looking to accept ACH payments from customers, using a dedicated payment processor, like Helcim, Square, or Stripe, can offer more flexibility and features than a traditional bank. Here’s why:

- Faster, easier setup: No need to go through a long bank approval process

- More tools to get paid: Accept ACH via virtual terminal, invoicing, or online payment pages

- Transparent pricing: No monthly fees, no contracts, no hidden costs

- Better support: Get real help when you run into issues with payments

How to set up ACH transfers for your business

If you’re eager to get ACH transfers going for your business, there are a few simple steps to follow.

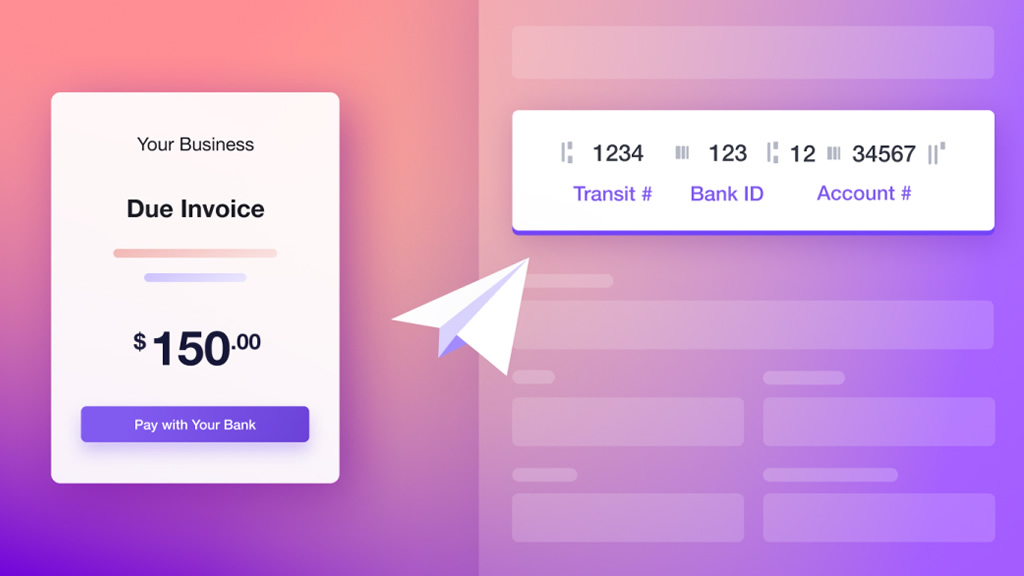

- Get client authorization: Find an ACH authorization template, or create your ACH pre-authorized debit authorization form and get your clients to sign it. This will authorize you to accept ACH payments from their account.

- Gather account details: Get your client to provide their bank routing and account numbers — you’ll need these in order to receive the payment. Just make sure to keep these secure as it is sensitive information.

- Schedule payments: Set up a recurring or one-time payment plan through your payment processor or bank.

Final Thoughts

Getting ACH services from banks is cumbersome and can take weeks to approve, and while there are ACH-only providers out there for merchants to choose from, using one processor for ACH and another for credit cards is likely more hassle than it's worth. ACH offers customers another convenient payment option and is cheaper than accepting credit cards for merchants. ACH is secure and works with a variety of payment tools.

If you're looking to accept ACH payments, give Helcim a call today!

FAQ about ACH transfers

Are ACH payments safe?

ACH is considerably safer than carrying cash around for large payments, and even safer than sending a check. When it comes to ACH payments, a customer only needs to enter their banking information or billing information once, so both customers and merchants know that money is going to the right place every time.

Because ACH payments do not work the same way as credit cards, they also do not have the same consumer protections or benefits credit cards do. For merchants, chargebacks are not something that happens regularly (if at all) as with credit cards.

Why do ACH transfers take so long?

ACH transactions go through a batch processing system that involves multiple verification and fraud prevention steps, contributing to the 1-5 business day processing time.

When do ACH transfers post?

ACH transfers typically post on the morning of the next business day if processed before the bank's cutoff time. Some banks provide early availability for incoming ACH credits.

Can you reverse an ACH transfer?

Yes, ACH transactions can be reversed under certain conditions, such as unauthorized transactions or errors. However, reversals must be requested within a specific time frame.

Do ACH transfers work internationally?

No, ACH transfers are only available within the U.S. For international transfers, options like SWIFT or wire transfers are required.

Are ACH transfers online payments?

Online payments are just a term to describe a business accepting payments via the Internet. ACH is a method of online payment. Most times you go to make an online payment, there will be an option to pay by credit card. ACH is just another payment method your business can offer at your online checkout point.

Related Articles

-

ACH Payment vs Wire: Which one is better?

Ryleigh Stangness | October 11, 2023

-

How can I accept online ACH payments?

Ryleigh Stangness | August 29, 2023

-

What is an ACH return and how much does it cost?

Ryleigh Stangness | November 24, 2022

-

Welcome to Helcim ACH Payments

Danny Randell | March 15, 2022