-

Content

Last Updated on September 9, 2025 by Robert Luong

Just like you get an invoice for a vet visit, a furnace repair, or your Amazon order, you also get one for your payment processing, your merchant statement.

The problem? These statements are harder to read than most invoices. They’re packed with fees, codes, and numbers that don’t always make sense at first glance.

Whether you’re concerned or just curious, every business owner can benefit from knowing how to read a merchant statement. Once you understand it, you’ll be able to:

- Spot where your money is really going

- Catch fees you shouldn’t be paying

- Hold your processor accountable

Plus, we can show you a few key terms, what to look for, and where to catch hidden fees, so you don't get swindled on your bill!

What is a merchant statement?

A merchant processing statement is a monthly report that your payment processor sends you. It lists every credit and debit card sale you accepted, then shows the portion that they take as fees before sending the rest to your bank. In other words, it’s like the bank statement for your card payments, money in, money out, and what you actually kept.

Depending on the provider, you might hear different names for this same document: merchant statement, merchant processing statement, credit card processing statement, merchant account statement, or simply processing statement.

Why do merchant statements matter?

I understand that it’s boring to look at all the abbreviations, tables, and numbers. That’s why many business owners spend only a few seconds glancing at their statements, just to check the summary of sales, fees, and leftover funds.

But that’s a mistake, because your merchant statement is more than just a receipt. It’s a financial control tool that helps you:

- See your true cost of card payments: Your merchant statement shows the real processing rates (effective processing rate) you pay, not just the advertised rate. We will show you how to calculate this real rate below. If you're interested, explore the cheapest credit card processing fees here.

- Catch errors and hidden credit card charges: Do you see fees you don’t recognize, such as “service fee” or “admin fee”? By reading your statement closely, you can spot these vague charges, question your processor, and stop overpaying.

- Spot fraud or unusual activity: If there’s a credit card chargeback, refund, or suspicious transaction, it will appear on your statement. A sudden spike in refunds or chargebacks can be an early warning sign of ongoing fraud that’s eating into your sales.

- Understand customer payment behavior: Reviewing your statement shows which card types your customers use most like Visa, Mastercard, Amex, debit, and others. If you notice more customers paying with expensive credit cards like American Express, you’ll also see your processing costs rise month over month.

- Hold your processor accountable: Your payment processor can promise one thing, but are they delivering? Your merchant statement reveals your true effective payment processing cost, including hidden costs like PCI fees, chargeback fees, and admin charges. If you spot a new fee or an overall increase you never agreed to, you have grounds to challenge it.

In short, reading your merchant statement is not optional bookkeeping — it’s a way to protect your bottom line.

Common merchant processing statement terms

| Term | What it means | Why it matters |

|---|---|---|

| Merchant Number | Your unique merchant account ID provided by the payment processor. | You’ll need this if you contact the support team for help with a payment issue. |

| Authorization | The step where the card is verified and funds are reserved. | If authorizations fail, the sale won’t go through. |

| Batch / Batching | A group of transactions (usually all sales for the day) submitted together for settlement. | Your statement often lists deposits by batch number, making it easier to match with your bank deposits. |

| Settlement | The process of moving funds from customers’ banks (issuers) into your bank account. | The statement lists deposits by settlement date, showing when you actually received funds. This makes reconciling with your bank statement easier. |

| Net Deposit | The actual amount transferred to your bank after refunds, chargebacks, and fees are deducted. | This is what appears in your bank account — not the gross sales figure. |

| Term | What it means | Why it matters |

|---|---|---|

| Interchange Fees | Fees collected by the customer’s bank. | Usually the largest portion of your cost. They vary by card type and how the card is used (in person or online). |

| Assessments (Card Brand Fees) | Small fees charged by card networks such as Visa, Mastercard, and American Express. | These fees are also non-negotiable. |

| Processor Markup | The processor’s cut, usually shown as a percentage (e.g., 0.30%). | This is the negotiable part of your costs. |

| Card Processing Charges | The total of interchange fees, assessment fees, and processor markup. | Shows the true cost you pay for each card transaction. |

| Authorization fee | A small fee charged each time a transaction is authorized. | Even if a sale doesn’t go through, you may still be charged this fee. |

| Batch fee | A fee charged each time you settle (close) a batch of transactions. | Important if you batch multiple times a day, fees can add up quickly. |

| Gateway fee | Monthly or per-transaction cost if you use an online gateway | Some payment processors charge extra cost if you add the payment gateway to your website. |

| Monthly Minimum Fee | If your monthly card processing fees don’t reach a certain threshold, the processor charges the difference. | If your contract includes this fee, check your statements carefully to avoid surprises. |

| Monthly statement/service fee | An administrative fee for generating and sending your monthly statement. | An unnecessary cost that you shouldn’t be charged for. |

| PCI DSS / PCI Compliance Fee | A monthly or annual fee tied to Payment Card Industry security compliance. | Entirely avoidable if you complete your PCI questionnaire on time. Otherwise, you may see a “non-compliance fee” of $20–$100 per month. |

| Equipment rental | A monthly fee if you rent a payment terminal or other hardware. | Recurring costs can add up quickly and become more expensive than buying equipment outright. |

| Term | What it means | Why it matters |

|---|---|---|

| Refund / Return | Money you refund to a customer. | This appears on your statement as a negative amount. |

| Chargeback Fees | When customers are not satisfied with a purchase, or believe they did not authorize it, they can ask their bank to reverse the transaction. If that happens, the sale is reversed and you are charged a fee. | This shows on your statement as a negative transaction amount, often between $15–$40. |

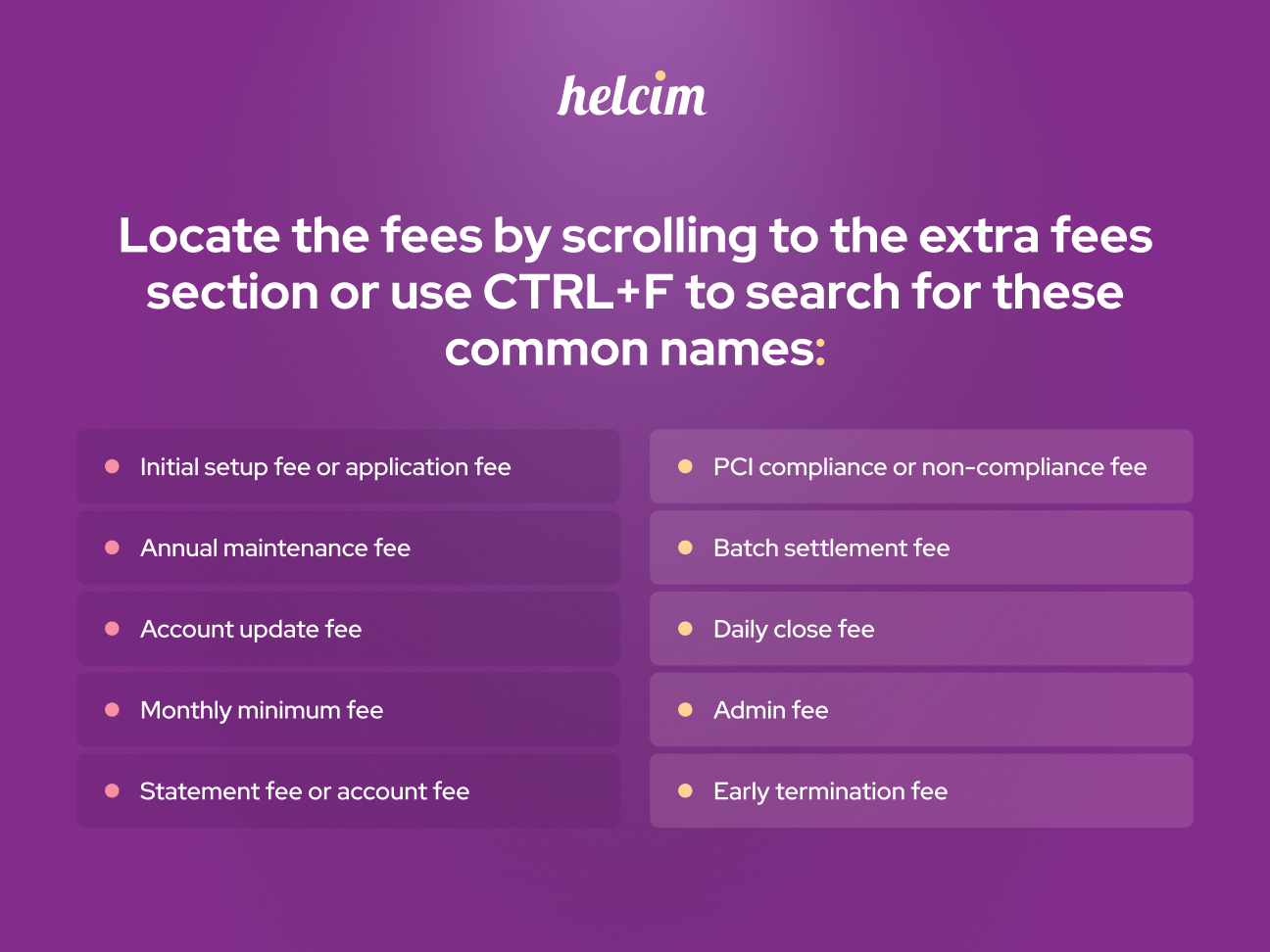

If you want to locate any hidden fees, simply use the combination of CTRL + F (windows) or COMMAND + F (Mac), then search for common terms like: maintainance fee, administration fee, minimum fee, termination fee, etc.

Common merchant processing statement abbreviations

| Abbreviation | Full term | What it means |

|---|---|---|

| VISA, VI, or V | Visa | Card network for Visa transactions. |

| MC | Mastercard | Card network for Mastercard transactions. |

| DISC | Discover | Card network for Discover transactions. |

| DISC NTWK FEE | Discover Network Fee | Discover’s version of an assessment fee. |

| AMEX | American Express | Card network for American Express transactions. |

| APF | Acquirer Processing Fee | A small per-transaction fee charged by Visa. |

| NABU | Network Access and Brand Usage | Mastercard’s per-transaction network fee. |

| TASF | Transaction Assessment Fee | American Express’s assessment charge. |

| INTCHG | Interchange Fee | Non-negotiable fee paid to the cardholder’s bank. |

| WATS AUTH FEE | Wide Area Transaction System Authorization Fee | A per-authorization network fee. |

| DIGITAL ENABLEMENT FEE | Digital Enablement | Fee for digital wallets like Apple Pay and Google Pay. |

| Abbreviation | Full term | What it means |

|---|---|---|

| DB | Debit | Transactions run as debit. |

| CR | Credit | Transactions run as credit. |

| RTN or RFD | Return / Refund | Money voluntarily refunded to a customer. |

| CHBK or C/B | Chargeback | A forced reversal by the cardholder’s bank. |

| AUTH | Authorization | The step where the card is verified. |

| AVS | Address Verification Service | Fraud check that matches billing address. |

| POS DEBIT | Point-of-Sale Debit | Debit transaction at the point of sale. |

| PIN DB / PIN DBBASE | PIN Debit | Debit processed using a PIN number. |

| Abbreviation | Full term | What it means |

|---|---|---|

| MID | Merchant Identification Number | Your unique merchant account ID. |

| TID | Terminal ID | The ID of your POS terminal. |

| MISC FEE | Miscellaneous Fee | A red flag for hidden charges. |

| ADMIN FEE | Administrative Fee | Another vague fee. |

| PCI | Payment Card Industry | Related to PCI compliance standards and fees. |

| SVC FEE | Service Fee | Processor or network service charge. |

What does your merchant statement include?

Every merchant statement looks slightly different depending on the provider, but they should include the 5 main sections:

| Section | What you learn |

|---|---|

| Account information and statement period | Who the statement belongs to and which dates it covers. |

| Merchant account summary | A big-picture snapshot: gross sales, refunds, chargebacks, fees, and net deposits. |

| Daily or batch summary | Line-by-line deposits for reconciliation with your bank. |

| Card type summary | Which cards your customers used, and which cost you the most. |

| Fee breakdown | Every interchange, assessment, and processor charge. |

| Chargebacks/adjustments | Details of any disputes or reversals. |

| Notices | Future changes to fees, terms, or compliance. |

1. Account information and statement period

At the very top, you’ll see your business name, address, merchant number (merchant ID), and the statement period (for example, July 1–July 31). This information tells you which billing cycle the statement covers. If you have any questions, you can call customer support and provide your merchant number when asked so they can quickly pull up your account.

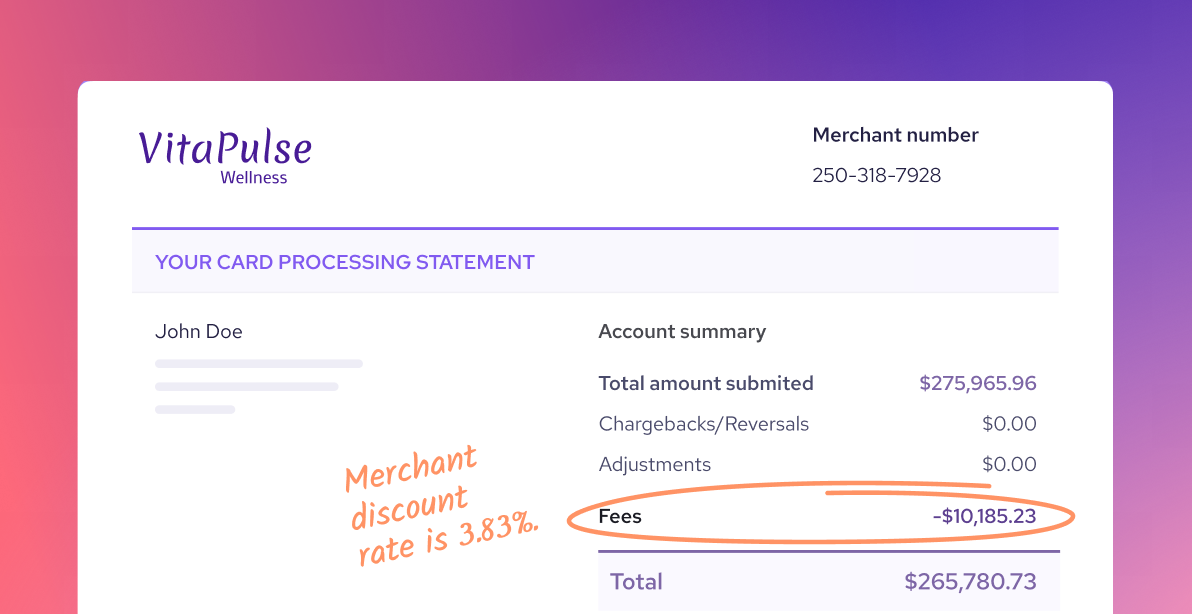

2. Merchant account summary (the snapshot page)

This is a quick overview of your monthly performance. It includes:

- Gross sales: The total value of all card transactions before refunds or fees.

- Refunds/returns: The total dollar value refunded to customers.

- Chargebacks/adjustments: The amount lost to disputes and other corrections.

- Total fees charged: All payment processing costs.

- Net deposits: The actual amount that you should receive in your bank account.

For example:

- Gross sales = $50,000

- Refunds = $1,000

- Chargebacks = $500

- Fees = $1,400

- Net deposit = $47,100

3. Daily activity or batch summary

This is the most detailed and often the most confusing part of the statement. It lists every payment processing batch that is closed each day. But what is a batch? Instead of processing and depositing funds into your account for every single transaction, payment processors group multiple transactions into a batch. They then process them all at once at the end of your business day.

In each line item, you should see:

- The date or batch number

- The total sales amount you processed

- Payment processing fees and other adjustments such as chargebacks or refunds/returns

- Any additional service charges such as admin fees or service fees

- The net amount deposited into your bank account

This section helps with reconciliation. You can match each day’s deposit in your bank statement to a specific batch on your merchant statement. If something is missing, you’ll know right away.

4. Card brand summary

Below the daily breakdown, you’ll find a section that shows the batches submitted by each card brand, such as Visa, Mastercard, Amex, or Discover. This summary helps you see which cards your customers used most on different days.

The card brand summary typically lists:

- The date of the submitted batch

- The batch numbers

- The total net dollar amount after processing fees for each card brand

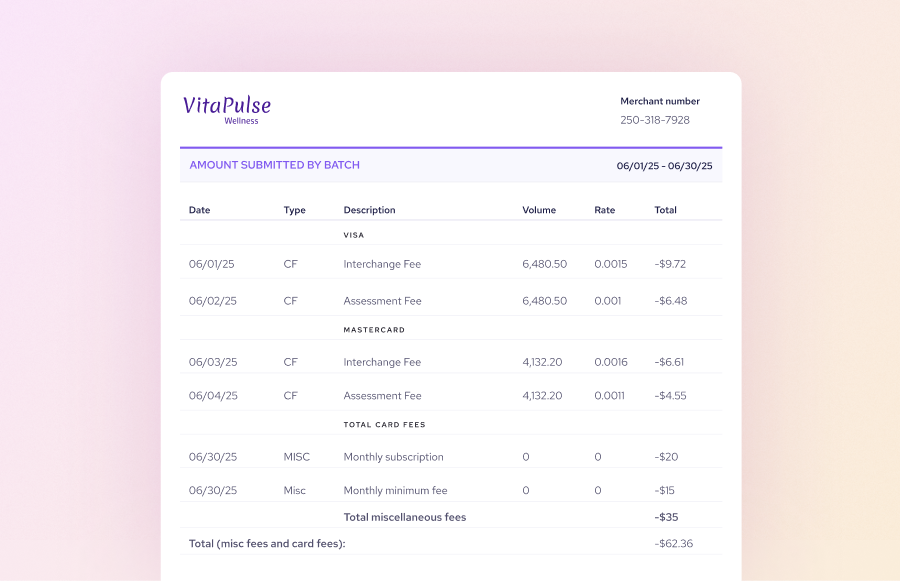

5. Fee breakdown each payment processing batch

This is the most detailed, and often the most confusing, part of the statement. It breaks down the total fees you pay by card brand.

Each type of fee is grouped under the card brand it relates to, such as:

- Interchange fees: Paid to the customer’s bank

- Assessment fees: Paid to the card network

- Processor markup: Collected by your payment processor

- Other per-transaction fees: Such as authorization fees, batch fees, or AVS checks

- Monthly or annual charges: Such as statement fees, PCI compliance, or equipment rental, collected by your processor

Why does this section matter? It gives you a detailed view of exactly what you’re paying. You can use the totals here to calculate your effective payment processing rate and see the true cost of accepting card payments. The formula is simple: Total fees ÷ Total sales = Effective rate

For example, last month, you processed $8,105 in sales, and the fee breakdown showed you paid $358 in fees. That means your effective processing rate was: $358 ÷ $8,105 = 4.42%. For your information, the cheapest payment processing rate is usually in the 2% to 2.5% range. So, if you are paying more than these rates, you’re overpaying.

6. Notices and messages

The final section is the notice or message from the payment processor. This section is usually found on either the first or last page of the merchant statement. Here, you’ll see upcoming changes to your merchant account, fees, or other important policy updates. Don’t skip these messages because they may have a significant impact on your revenue in the long term.

How to use the merchant statement to know your true payment processing rates

Using the merchant statement, you can calculate your true payment processing rate (a.k.a effective payment processing rate). It tells you the true cost of accepting card payments, regardless of what your processor “advertised” when you signed up. Aside from the payment processing fees, the effective payment processing rate takes into account other fees like PCI fees, batch fees, administrative fees, etc.

Effective payment processing rate (%) = (Total fees ÷ Total sales volume) x 100

Example on how to calculate your effective payment processing rate: Let’s say your business processed $20,000 in sales across 400 transactions in a month. Here’s how fees could look:

- Interchange = $360

- Assessments = $28

- Processor markup = $120

- Batch fees = $6

- Monthly subscription fee = $30

- Service fee = $10

- Admin fee = $8

Total fees = $360 + $28 + $120 +$6 + $30 +$10 +$8 = $562

Your effective rate = $562 ÷ $20,000 = 2.81%. So if payment processors advertise that they charge you 2.50%, then you are actually paying more than you promised when you take into account other hidden fees like batch fees, service fees or admin fees.

How to identify chargebacks and refunds in a merchant statement

Refunds and chargebacks are two different events that both reduce your revenue.

A refund (sometimes called a return) is when you voluntarily send money back to a customer. Refunds may also be labeled as RTN or RFD. In your merchant statement, refund amounts typically appear as negative amounts in the sales or batch summary.

A chargeback is different. It’s when the customer’s bank forcibly reverses a transaction because the cardholder disputes it. In your statement, chargebacks are labeled as CHBK or C/B. They appear as negative amounts with a reference code or masked card number. You’ll also see a chargeback fee ($15–$40) as a separate line in the fee breakdown.

For Helcim merchant, if they dispute the chargeback successfully, Helcim will refund a chargeback fee.

Common mistakes when reading merchant processing statements

Merchant processing statements can be overwhelming. So, it’s understandable that many business owners only skim them quickly or avoid looking at it. But without reading it, you face the risks of paying more than you’re promised.

Here are the most common mistakes business owners make when reading merchant statements, and how to avoid them.

1. Confusing “discount rate” with a real discount: The term merchant discount rate often tricks business owners into thinking they are getting cheap payment processing fees. In reality, it’s just another term for payment processing fees.

2. Trusting the summary without checking the details: Many processors bill some fees later (like interchange adjustments, monthly service fees, or assessments). That means part of August’s fees might actually show up on September’s statement.

3. Ignoring vague fees: Many processors bury hidden or vague credit card fees deeper in the statement or push them into the following month’s billing cycle. These can be labeled as “service fee,” or “administrative fee,”. So, make sure to question your payment processors when you see these vague fees shown in your merchant statement.

4. Not comparing month-to-month: Make sure to compare your payment processing fees this month to last month to spot overall trends. If your sales haven’t increased much but your processing fees have, it’s time to ask why. Is it because more of your customers are using rewards cards? Or did your payment processor raise its fees?

5. Overlooking chargebacks and refunds: Some merchants forget to review the chargebacks or refunds. Refunds and disputes reduce your revenue, and chargebacks come with extra fees. If you don’t catch them, you won’t be able to spot the fraudsters or underlying problems of your product.

6. Skipping the fine print and notices: The last page of a merchant statement often contains “messages” from the processor. This is where they announce upcoming fee increases or policy changes. If you miss it, you’ll be surprised when fees go up.

How to reconcile merchant processing statement with your bank statement

Now you know how much processing fees you pay and how much ends up in your bank statements. But how do you check if you receive the actual amount that the merchant statement claims to send you? This is when the reconciliation process comes into play.

Below are the 4 steps to reconcile the merchant processing statement with your bank statement.

Step 1: Start with your daily batches or deposits

Most merchant statements include a section that breaks down batch processing by date, or multiple times per day if you close your batch more than once. Look for headings like Daily Activity, Batch Summary, or Deposit Detail.

In this section, you’ll typically see line items showing:

- The date the batch was closed

- The total sales

- Refunds

- Total fees

- The net deposit amount sent to your bank account

Step 2: Match statement deposits to bank deposits

Now open your bank statement and look for deposits that match the net deposit amounts on your merchant statement. Important: Funds may take 1–3 business days to post to your bank account.

If you don’t see the deposit on the same day you closed your batch, check your bank statement 1–2 business days later to avoid missing it. Learn more about payment processing times here.

Example:

- Batch on Sunday, July 16: $4,000 net deposit

- Bank deposit shows up on Monday, July 17: $4,000

Step 3: Account for monthly or yearly fees

Not all fees are deducted daily. Some processors take them out at the end of the month or year. Common monthly and yearly fees are subscription fees, PCI compliance fees, and monthly minimum fees. So if, in any month, you notice that the money deposited into your bank account is suddenly lower than usual, check your merchant statement for monthly or yearly fees that may be cutting into your sales.

Step 4: Reconcile refunds and chargebacks

Another reason you might see lower-than-usual deposits in your bank account is refunds and chargebacks. First, check if you issued a large number of refunds to your customers. If so, confirm whether this was due to product quality or operational problems in that period.

For chargebacks, if you notice a sudden increase in chargeback fees, it means your business has been hit with more fraud. In this case, make sure you have systems in place to prevent fraudulent transactions, and be especially cautious with unexpected large purchases.

Helcim can help you read your merchant statement

If your merchant statement feels too confusing, Helcim can help you review it and spot any hidden payment fees. We started as a small business ourselves, so we know how important it is to grow without being taken advantage of. That’s why this service is completely free. No strings attached, just honest help to make sure you’re not overpaying your processor.

Here’s how it works:

- Book a call, and our specialists will analyze your payment statement.

- We’ll uncover any hidden fees and show you how much you might be overpaying.

- You’ll get expert tips on how to cut costs and see how much you could save by switching to Helcim.

Related Articles

-

Understanding payment processing time for your business

May Montenegro | October 29, 2024

-

What are the lowest credit card processing fees?

Robert Luong | September 11, 2024

-

How to implement surcharging: A step-by-step guide

Jared Slemp | August 22, 2024

-

Credit Card Processing Fees Ultimate Guide

Ryleigh Stangness | July 1, 2022

-

5 hidden credit card fees you must avoid

Nic Beique | June 29, 2022