-

Content

Last Updated on October 21, 2024 by Robert Luong

Accepting credit cards have transformed from a “nice to have” for your business into the most popular and expected payment method. In fact, credit card transactions account for 32.6% of consumers' monthly payments. As a result, it's crucial for businesses to accept credit card payments to ensure they capture every sale and meet customer demand.

However, not all credit card processing companies are created equal—especially when it comes to costs. For most businesses, price is a top consideration. In this article, we'll break down the two main pricing models, flat rate and interchange plus, so you can find the one that fits your business best.

The ultimate guide to accepting credit cards.

Discover essential knowledge and industry insights to increase your bottom line.

What makes up credit card processing fees?

Before we dive into the difference between flat rate and interchange plus pricing model, it’s important to know the components that make up the credit card processing fees.

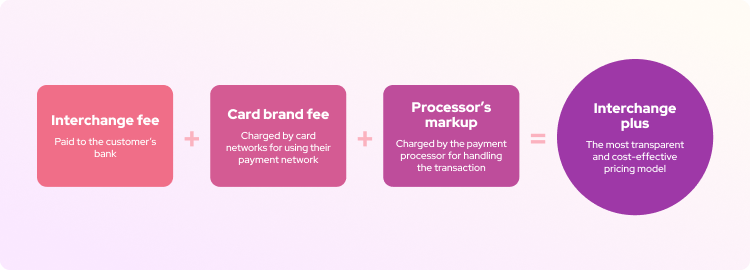

Credit card processing fees might sound complicated, but they’re made up of three simple parts: interchange fees, assessment fees, and the processor margin.

-

Interchange fees are set by the card networks like Visa or Mastercard, and they are paid to the bank that issued your customer’s credit card. Think of it as a fee for the risk the bank takes on lending out money and approving the transaction.

-

Assessment fees are small charges paid to the card networks for making sure the whole processing network runs smoothly. It’s a lot smaller than the interchange fee, but it’s still part of the total processing cost.

-

Processor fixed markup is where your credit card processing companies make money. They add their own markup on top of interchange and assessment fees for handling the credit card transaction.

Out of the three components above, interchange fees are the ones that fluctuate with every transaction. The reason? Card brands like Visa and Mastercard treat different types of credit card transactions differently. For example, an in-person purchase has a much lower risk than an online one, and different card types (like rewards cards) come with their own fee structures.

Because of this, your actual credit card processing fees can vary from one transaction to the next, and your cost per transaction will be dependent on how your payment processor decides to pass on those fees to you. The two most popular fee structures are Interchange Change Plus and flat rate pricing. Let's unpack those both and find out what is the best choice for your business.

What is interchange plus pricing and how does it work?

With the interchange plus pricing structure, the credit card processors pass you the true cost of each transaction and add a transparent markup on top.

This means, whenever you process a transaction that is eligible for a lower interchange fee you will be saving money. When you process a card with a higher interchange fee (like AMEX), the credit card processor will charge higher fees compared to other card brands like Visa.

The pros and cons of interchange plus pricing model

Pros of interchange plus pricing model:

- Transparency: Interchange-plus pricing gives you a clear breakdown of all fees on your monthly merchant statement, letting you see exactly what you’re paying for each card and transaction type.

- Cost-effectiveness: Unlike flat-rate pricing, where you pay the same fee for every transaction, interchange-plus passes you the true cost. This ensures you’re not overpaying for lower cost credit card transactions.

- Savings are passed to you: When card brands lower interchange rates, interchange-plus pricing passes those savings directly to you.

- Scalability: As your business grows, interchange-plus processors like Helcim automatically reduce your transaction fees based on increased volume. The more you process, the more you save, making interchange-plus ideal for scaling your business.

Cons of interchange plus pricing model:

- Fluctuations: Since interchange fees fluctuate on every transaction, your payment processing fees will fluctuate with each transaction. This can make it harder to accurately forecast your monthly processing costs.

- Complexity: The breakdown of fees into interchange, card brand fees, and the processor's markup can be more difficult to understand. As a result, businesses need to carefully review their statements to understand what they’re being charged.

What is flat rate pricing and how does it work?

Because interchange fees fluctuate, many credit card processing companies simplify things by charging a flat fee for every type of credit card payment. For example, they might charge 2.5% for in-person credit card payments and 3% for online.

With flat rate pricing, the type of credit card your customer uses won’t change your cost. Whether they’re using a rewards card, a business card, or a basic credit card, you’ll always pay the same rate. This makes the flat rate pricing model easy to understand.

The pros and cons of flat-rate pricing model

Pros of flat-rate pricing model:

- Simplicity: With flat-rate pricing, you always know what you're paying. No matter what type of card the customer uses, the fee is easy to understand.

- Predictability: By paying a flat fee, you can easily plan and forecast your processing costs, giving you more control and confidence in managing your finances.

Cons of flat-rate pricing model:

- Higher costs for lower-risk transactions: The credit card processor often sets the flat fee high enough to ensure the processor’s profitability. This means you could end up overpaying on low-cost transactions.

- Lack of transparency: Card brands periodically adjust interchange fees, and when they increase, flat-rate processors increase their fees to protect their margins. But when interchange fees go down, many processors keep their rate unchanged, pocketing the difference instead of passing the savings to you. For example, in October 2024, The Globe and Mail reported that Stripe would not lower its merchant fees, despite Ottawa’s agreements with credit card firms to reduce fees for businesses.

- Lack of scalability: Flat-rate pricing doesn't scale with your business. Whether you process $100 or millions in transaction value, the rate remains the same, resulting in hefty fees even as your sales grow. This model doesn't reward businesses for scaling and can lead to higher costs as you expand.

Why are merchants choosing interchange plus over flat rate pricing model?

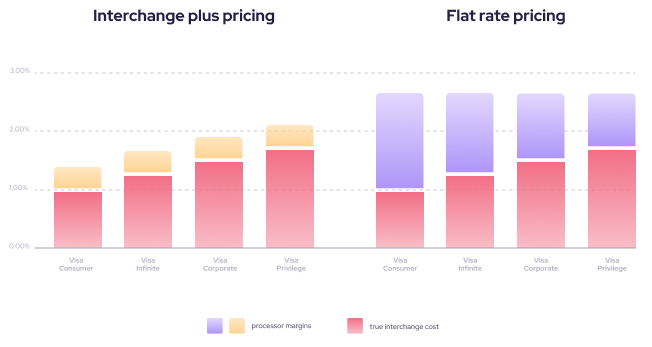

Interchange-plus pricing is attractive to many merchants because most credit card payments involve cards with lower interchange rates. The average customer isn’t using high-end cards like an Amex Black or Visa Infinite Privilege; they’re more likely carrying a standard, low-fee credit card with a lower interchange rate. This means you often benefit from lower transaction costs with interchange-plus.

A key advantage of interchange-plus is transparency. While flat-rate pricing has a fixed, often high markup, interchange-plus clearly separates the interchange fee and processor margin. This gives you a clearer view of costs and often results in lower overall fees for merchants compared to flat-rate pricing.

What is the typical interchange plus rate?

Helcim offers 25% lower credit card fees on average compared to other flat-rate credit card processing companies like Moneris, Square, Clover, or Stripe.

Helcim Interchange Plus compared to other flat rate processor for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Helcim Interchange Plus compared to other flat rate processor for Canada businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards* + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

How much can you save with interchange plus vs flat rate?

Interchange-plus pricing is the most cost-effective option for many businesses. Below are the average savings businesses in different industries have seen with Helcim’s interchange-plus pricing compared to flat-rate processors in 2024.

| Industry Market | Total Savings (%) |

|---|---|

| Automotive | 28.31% |

| Cab & Delivery | 27.14% |

| Charity & Non-Profit | 31.04% |

| Contractors & Home Services | 26.37% |

| Education | 33.09% |

| Enterprise & Utilities | 48.45% |

| Financial Institution | 24.40% |

| Gas Stations | 40.54% |

| Government | 41.54% |

| Health, Beauty & Wellness | 31.62% |

| Healthcare | 25.09% |

| Hotels & Lodging | 23.36% |

| Online Sales | 20.66% |

| Organizations & Associations | 27.06% |

| Platforms, Apps & SaaS | 20.20% |

| Professional Services | 27.68% |

| Recreation | 27.01% |

| Restaurant | 31.49% |

| Retail Goods | 25.00% |

| Transportation | 20.36% |

| Wholesale | 23.23% |

The data presented above is sourced from Helcim’s internal analysis, comparing Helcim’s fees to the market average for flat-rate pricing.

Save 25% on credit card fees with Helcim interchange plus

Overall, interchange-plus pricing is the smarter choice for most businesses. It lets merchants benefit from lower interchange rates while keeping the processor's margin transparent and minimal.

If you’re looking to reduce your credit card processing fees, sign up with Helcim today or contact us to learn how much you can save.

If you're ready to switch but tied to your current provider, Helcim’s Merchant Buyout Program offers up to $500 in credits to help cover contract cancellation or equipment costs. Plus, we’ll guide you through the entire process—from handling the paperwork to migrating your data seamlessly to Helcim.

Break up with bad rates.

Feeling stuck with your provider? We'll waive $500 of your processing fees when you switch to Helcim.

Related Articles

-

Level 3 and level 2 credit card processing: How much can you save?

Robert Luong | September 30, 2024

-

Best Credit Card Processor for Small Businesses

Robert Luong | June 20, 2024

-

Free Credit Card Processing: Meet Helcim Fee Saver

Ryleigh Stangness | June 26, 2023

-

7 Surprising Benefits of Accepting Credit Cards

Ryleigh Stangness | January 24, 2023

-

Credit Card Processing Fees Ultimate Guide

Ryleigh Stangness | July 1, 2022

-

5 hidden credit card fees you must avoid

Nic Beique | June 29, 2022

-

Interchange fees ultimate guide A-Z

Miranda Russell | April 3, 2022

-

How credit card processing works: An ultimate guide

Danny Randell | March 3, 2021