-

Content

Last Updated on May 2, 2023

Convenience Fee Meaning: What it is and how it works

"How would you like to pay?"

It turns out this can be a loaded question. Depending on your answer, you might notice an item listed after the subtotal, "convenience fee @ $1.50," for example. What does that item listed on your invoice mean, and why do merchants charge them?

This article will explain why and how some merchants charge a convenience fee, and the difference between a convenience fee and a surcharge fee. We will dive into questions like what transactions and payment methods charge a convenience fee, their legality, and how to navigate them.

Key takeaways:

-

A Convenience fee, also know as a service fee, is different from surcharges- convenience fees are applied by payment channel, and there are specific stipulations merchants must follow.

-

Convenience fees are usually applied to card-not-present, credit card payments, or online transactions and invoices/ virtual terminals.

-

Convenience fees are legal almost everywhere in Canada and the U.S. (although merchant pressure has led service providers such as Mastercard to "modify certain standards and business practices to permit Canadian merchants to apply an extra checkout fee" as early as October 2022.)

-

A few ways merchants can mitigate charging convenience fees include raising prices, offering cash or debit discounts, processing in-person payments instead, and switching providers to take advantage of lower interchange rates.

Why are convenience fees charged?

When a customer uses a credit card to make a purchase, specific fees called processing fees. are associated with the transaction, usually out of the merchant's pocket and paid to credit card companies. These fees can add up, increasing operating costs for many business owners.

Merchants have avoided being subjected to these costs when a customer pays by cash (at least that is the perception, although there are many other costs associated with taking paper money or coins) and usually pay lower flat fees for debit transactions and ACH transactions.

However, since the pandemic, consumer trends are rapidly gravitating towards contactless credit card payments. Cash is not as appealing as it once was, nor as standard (who carries grimy coins around anymore- even laundromats take tap now) and setting up ACH payments can seem a bit more tedious than a credit card numbers.

With the added incentive of rewards programs with credit card providers, merchants have to adapt to accommodate customer preferences. While cardholders benefit from using a credit card and the rewards programs that often accompany them, merchants benefit from increased sales and customer satisfaction. However, pricing models such as flat rates and legacy processors with hidden extra fees can make accepting credit cards costly for merchants.

In addition, specific payment methods such as online, keyed, virtual terminals, and invoices can all lead to higher costs in time and fees with outdated POS systems or software, which merchants understandably want to avoid.

To make up for this cost, merchants sometimes charge a convenience fee, or service fee meaning an extra fee to cardholders when using specific payment methods such as making credit card payments. In doing so, they must also offer, thereby incentivizing customers to pay via an alternate payment channel such as ACH payments for example.

Convenience fee vs surcharge fee

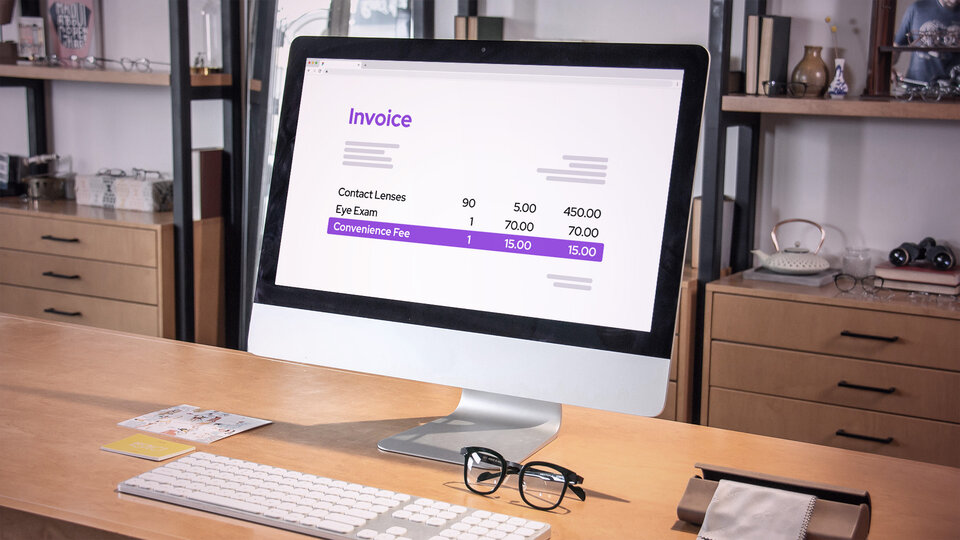

Businesses will sometimes charge a convenience fee as a small expense tacked on to the cost of a transaction amount to cover a merchant's processing fee or inconvenience (or some of it, as there is a capped amount they can recover.)

It's easy to mix up a convenience fee with surcharges because they are pretty similar. They both serve the same purpose but are executed slightly differently. A convenience fee is fee charged for the convenience of a transaction type such as online.

On the other hand, a percentage-based surcharge is applied to a specific card brand type. For example, taxes are applied to all card types of a particular brand (i.e., Visa Gold, Visa Infinite). They are more often charged across brands such as Visa and Mastercard- partly due to non-competition clauses which state that you must set fees for all brands equally.

Read more about surcharge fees and how they affect merchants and cardholders.

Which payment methods are common to charge convenience fees?

Now that we've explained how convenience fees are applied to specific payment methods let's discuss which ones are the heavy hitters for merchants such as a credit card payment (and where to look out.)

In an internal survey at Helcim, we asked merchants which payment methods they would likely apply a convenience or surcharge fee to if we integrated this as a new feature.

We found that 24% of merchants would apply it for invoicing.

The name is a dead giveaway: convenience fees.

It is all about convenience (for merchants, too) while covering their costs.

As much as merchants want flexible and convenient payment options for their customers, hopefully encouraging more sales, they are also looking to minimize costs.

We've all heard time is money. Transactions that require more time and energy, for example, legacy processors, outdated POS systems, or a clunky e-commerce site, are a considerable time and resource suck. (Read: critical components of a successful online store) Switching payment processors, upgrading your POS system, and using integrated built-in eCommerce capabilities like the Helcim online store is also a few of the ways to streamline your operations. However, many merchants may apply a convenience fee to cover the expense, if not simply to discourage consumers from using that particular payment method. Some payment processors will even overcharge merchants to access online tools (unlike Helcim), which is often a factor in avoiding specific payment channels or charging convenience fees to recoup the cost.

How much can a merchant charge for a convenience fee?

The most common transactions charged with a convenience fee include (you guessed it) online and invoice transactions. So how much are merchants charging, what are the legalities surrounding convenience fees, and how is a convenience fee calculated?

The answer: A merchant must follow specific rules and guidelines to implement a convenience fee. These rules include:

Merchants can either charge a flat fee or a percentage.

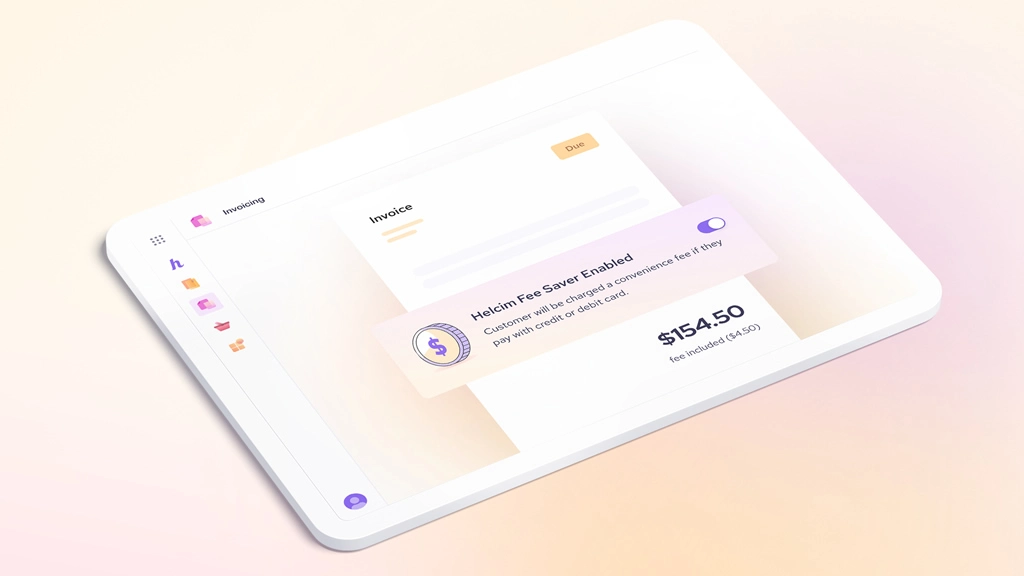

That fee must be disclosed clearly at the storefront (or website payment page) and at the transaction time (listed as a separate itemized cost on the payment terminal or invoice.

Customers must be given an option at the time of payment to decline the convenience fee without repercussions and swap their payment method.

If you want to know more about Canadian legalities, you can find out more eligibility information here.

How can I mitigate convenience fees?

Other options to mitigate charging convenience fees to your cardholders as a merchant are accessible. Here are a few of the ways merchants in the U.S. and Canada avoid charging a convenience fee and how they are making up the cost (or not in some cases.)

The cost of doing business: Eating the cost of processing fees

In our survey results, some merchants expressed that eating the cost of the transaction or inconvenience was simply the cost of doing business. Others have found ways around charging convenience and surcharge fees without taking a hit to their bottom line.

Making up the difference: cover the cost without charging a convenience fee

1. Minimum Purchase Requirements

Enforcing a minimum purchase requirement on your customers is not the same as a convenience fee. However, it is a way to offset the cost of processing fees or using credit cards for small transaction sizes.

For example: Suppose your payment processor has a flat rate or interchange-plus pricing structure. In that case, you'll be charged a specific rate on every transaction plus so many cents (e.g., 2.9% + 8 cents per transaction plus the convenience fee of $1.50, for example. Suppose you process a transaction that's only in a dollar amount. You'll lose a lot of processing (especially when given the $0.08 authorization fee). However, on a five-dollar transaction, this authorization fee has a much smaller impact on the overall cost-benefit for that transaction.

2. Creative ways to make up the revenue of convenience fees

- Increase your prices on your products/services to compensate for credit card processing fees (as a general number, say approx. $1.50)

- Switch processors, so you're paying less in processing fees (e.g., from flat rate to interchange plus)

- Process in person rather than online to save on processing and not have to pass the additional cost on to your customers

3. Motivate your customers to use another method via discounts Lastly, merchants (especially Canadians) will offer a discount for using a particular payment method rather than a fee. Discounts are usually applied to cash transactions because it saves the merchant from incurring the initial credit card (or Debit in the U.S.) fees in the first place.

Convenience fees: conveniently summed up

Now that you know about credit card convenience fees, you know how merchants charge them, how to look out for them as a consumer, and how merchants can mitigate this cost for their customers. You might be wondering what the best option for you and your business is.

Pros of convenience fees: -Recoup costs of time, resources, and credit card fees -A small cost to the customer that helps the merchant keep their operating costs down -May discourage a customer from using what may be an inconvenient payment channel in the first place

Cons of charging convenience fees: -survey respondents express hesitancy to implement convenience fees in fear of resentment and flack from consumers over excessive after-the-fact fees -customer distrust or discontentment -rules and regulations dictate who, how and where merchants can implement convenience fees (may not be an option for your business depending on your state law or industry)

In conclusion:

Offering flexible payment methods gives you an advantage as a merchant to accept payment and facilitate payment (simple math: more sales= more profits for your business) hence the appeal to accept credit card payments. This inevitably creates challenges with expensive credit card fees or huge time sucks for dealing with online invoices in an old POS system, for example. Thus the need for compensation may impact your costs.

By passing on your credit card processing fees to your customers, you will be able to recoup some of these costs. However, given the sensitive nature and the negative impacts this may have on customer experience, satisfaction, and trust merchants need to follow best practices on whether to pass on credit card fees to their customers and doing so in a transparent and seamless way.

Related Articles

-

Credit card surcharge: What is it and how to implement legally?

Dan Chong | November 13, 2023

-

Free Credit Card Processing: Meet Helcim Fee Saver

Ryleigh Stangness | June 26, 2023

-

Are Payment Processing Fees Tax Deductible?

Ryleigh Stangness | March 28, 2023

-

How to reduce your credit card processing fees

Ryleigh Stangness | November 1, 2022

-

Credit Card Processing Fees Ultimate Guide

Ryleigh Stangness | July 1, 2022

-

5 hidden credit card fees you must avoid

Nic Beique | June 29, 2022

-

How credit card processing works: An ultimate guide

Danny Randell | March 3, 2021